Reinforcing Gas Security of Supply Following Ukraine’s Invasion

What Measures at What Cost?

-

abril 20, 2023

Downloads Download Article

Download Article

-

Executive summary

Following Russia’s invasion of Ukraine, and the subsequent collapse of Russian gas supply to Europe, most European governments swiftly enacted new measures aiming at reinforcing their security of gas supply. FTI Consulting conducted a review of such government measures assigned to gas market players,1 aimed at reinforcing security of gas supply in Europe. We have identified 23 major new measures implemented since the beginning of the war in Ukraine.

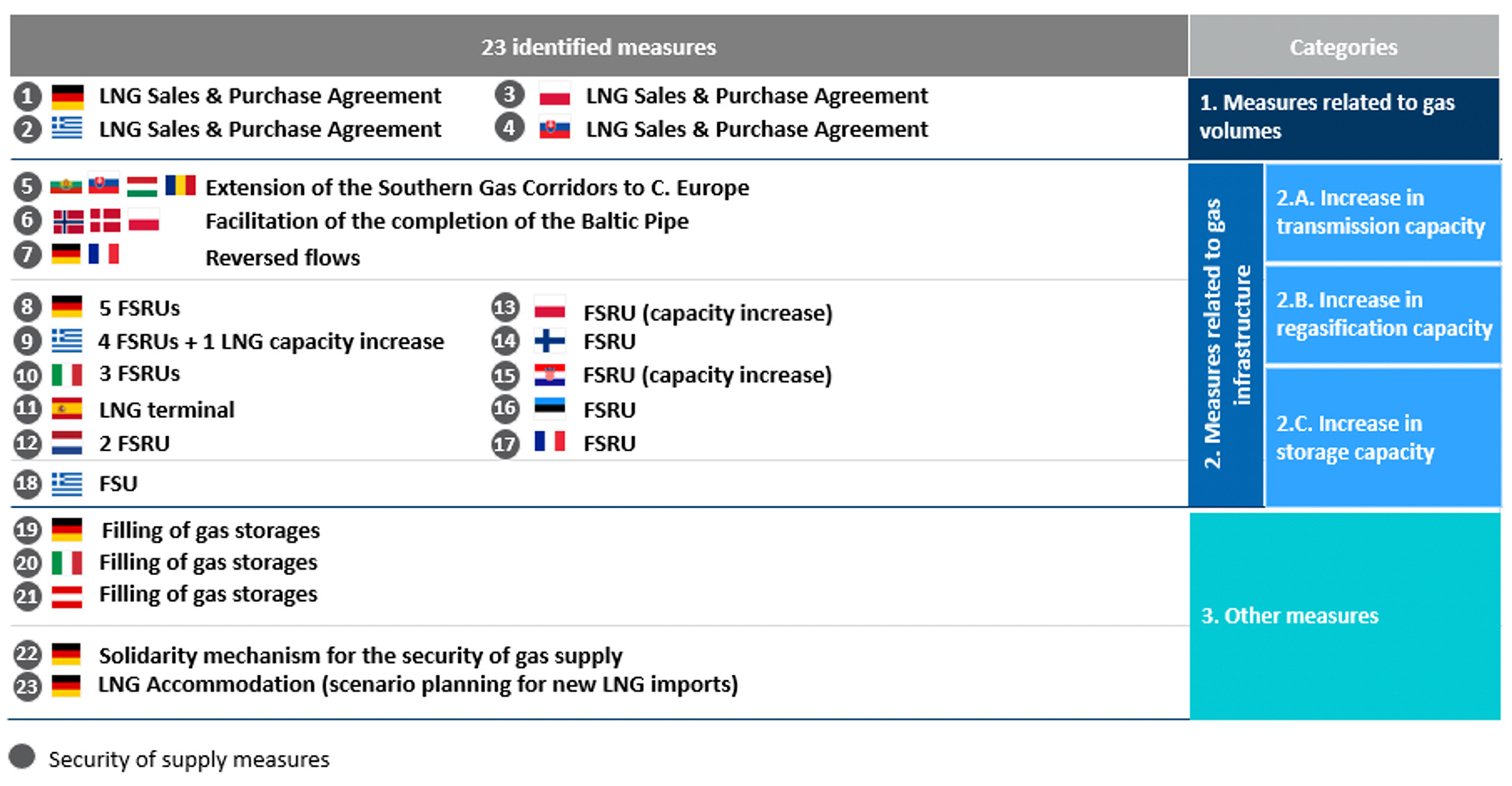

Among the 23 identified measures, 14 of them were focused on gas infrastructure enhancement, notably to increase LNG regasification and storage capacity, and gas transmission capacity. In the remaining 9 measures, the most prominent were contracting new non-Russian gas supply and ensuring the filling of existing gas storage facilities.

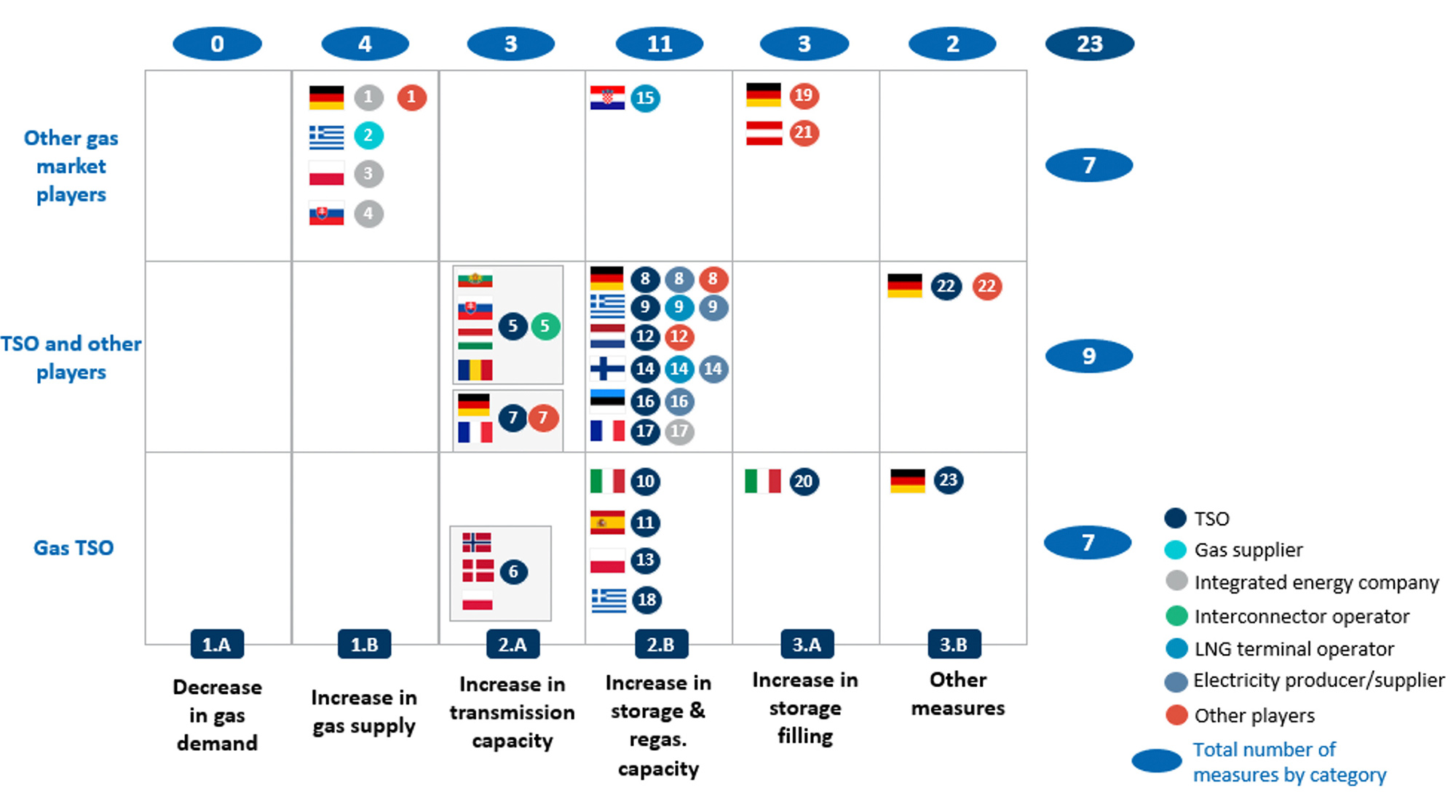

European governments tasked various organisations to implement the new security of supply measures, with no common approach across the bloc. Apart from supply contracting measures which were all carried out by national gas utilities, government-mandated measures were implemented by either transmission system operators (TSOs) or other gas market players, but with no consistency across countries.

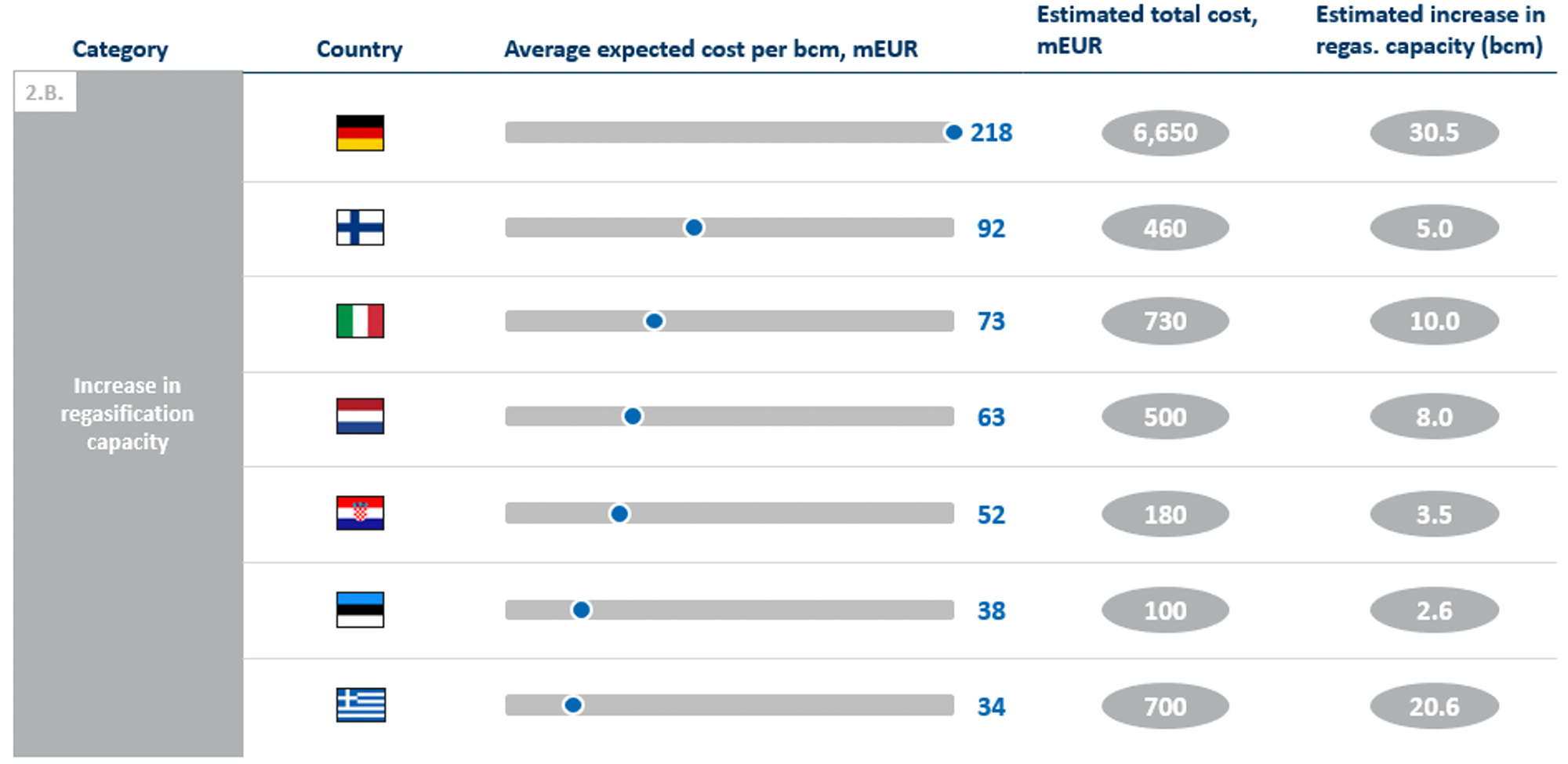

Costs of measures also varied from one country to another. Zooming on the costs of new LNG regasification capacity, we note that the German government paid the highest average cost per billion cubic meter (bcm) of added annual capacity (218m€/bcm), which is more than three times the cost incurred in the neighbouring Netherlands (63m€/bcm).

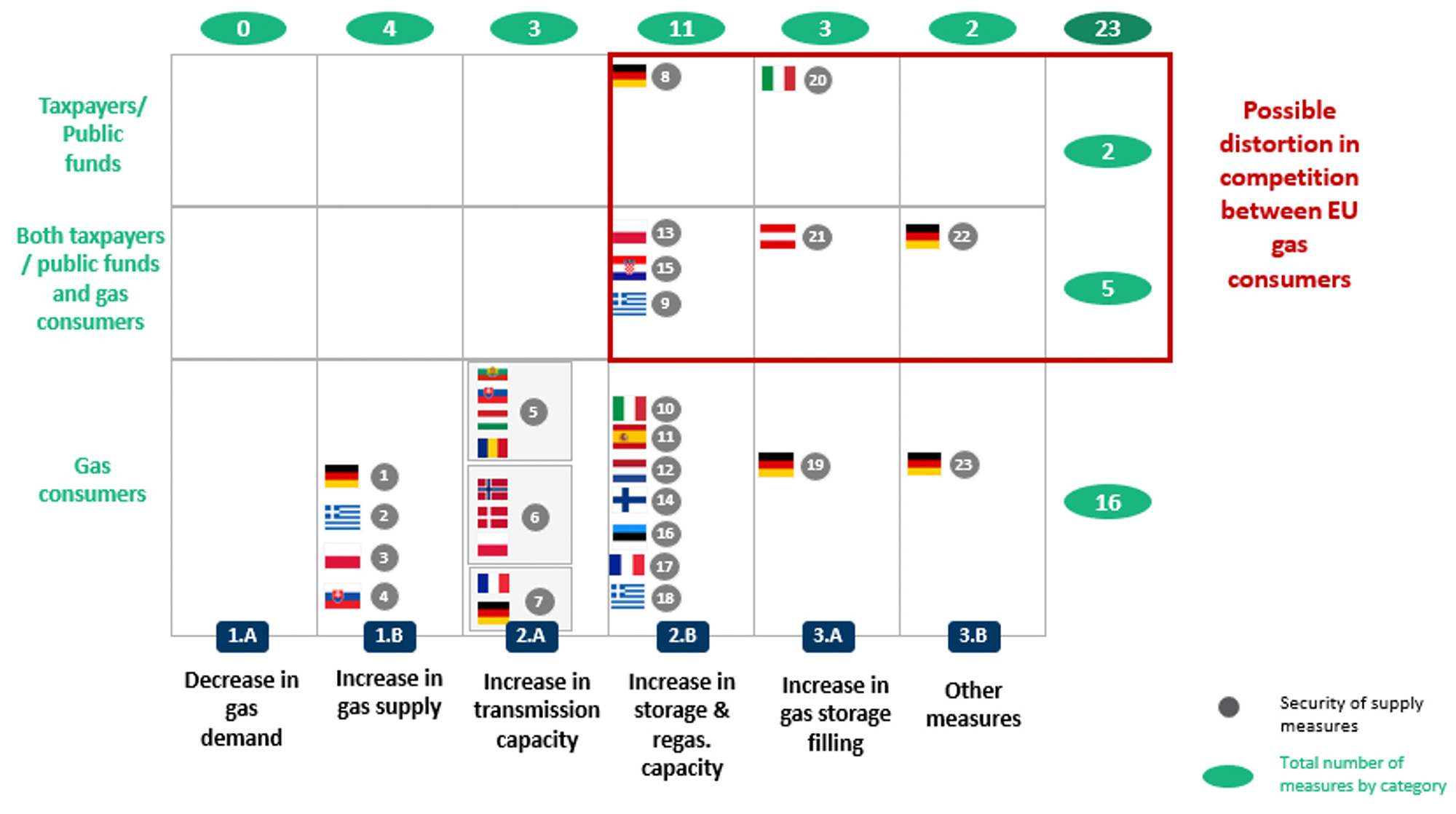

In general, the costs of the government measures to support gas security of supply are borne by gas consumers through increased network tariffs and/or increased specific gas consumption taxes. However, six countries, including Germany, Italy and Poland, are also using taxpayer support to finance the measures, possibly leading to some distortions in the single gas market due to uneven subsidization.

Governments have focused on increasing LNG regasification and storage capacities

Out of 23 identified gas security of supply measures implemented post Ukraine’s invasion, 14 of them are related to enhancement of gas or LNG infrastructure capacities. Increasing LNG regasification capacity was the most popular measure assigned by 10 governments (including Germany, Greece, Italy, Spain and the Netherlands) that resulted in the leasing of a total of 17 Floating Storage and Regasification Units (FSRUs) and the increasing of capacity at two existing FSRUs and two LNG non-floating terminals, thereby adding 100 bcm2 to the European annual regasification capacity. Moreover, DESFA, the Greek TSO, was tasked to increase the existing LNG storage capacity by chartering a Floating Storage Unit (FSU) for a period of 12 months. Regarding gas pipeline infrastructure, the new measures included the increase of transmission capacity on the extension of the Southern Gas Corridor towards Central Europe to 20 bcm/year, the facilitation of the construction of the Baltic Pipe connecting Norway-Denmark-Poland with a capacity of 10 bcm/year and the activation of reversed flows between France and Germany.

Figure 1: Overview and classification of identified measures

Source: FTI Consulting analysis3

There was no common approach by governments in measure implementation

Out of five categories of identified measures (Figure 1), the increase in gas supply through contracting of new non-Russian volumes was the only measure where similar entities have been in charge of implementation (nationally-focused gas utilities). To a certain extent, a common approach was also maintained for the expansion of transmission capacity, where gas TSOs led the implementation, but with significant implication from interconnector operator or other market players in some cases. However, in all others measures, including LNG storage & regasification capacities increase and storage fillings, no unequivocal trend concerning the entity in charge was observed: both TSOs and other players were tasked to implement the measures.

Figure 2: Benchmark of the identified measures by party responsible for the implementation

Source: FTI Consulting analysis

The costs of security of supply measures have varied, with Germany paying 2.5x the European average unit cost for regasification capacity additions

Among the different measures, we were able to carry out a comprehensive benchmark only for costs linked to the addition of regasification capacities, due to other cases being limited by confidentiality or specificity. We estimated that the costs for the German government reached in average 218 million EUR per each bcm of added regasification capacity,4 which is about 150% more than the European average and more than six times the cost of regasification capacity expansion in Greece where the estimated costs incurred per extra bcm was 34 million EUR.5

Figure 3: Benchmark of the increases in regasification capacity by expected costs6

Source: FTI Consulting analysis

The cost of new measures has been borne by gas users in most countries, but also by taxpayers in six countries, creating potential distortions of competition

In most cases, governments have requested gas consumers to bear the costs of the new measures. But while gas consumers are exclusive bearers of the costs of increases in gas supply & transmission capacity development, governments have used taxpayers’ support for the measures related to increase in LNG storage and regasification capacity, and gas storage fillings. For instance, in Germany, the increase of regasification capacity through FSRUs is exclusively paid by taxpayers, while similar costs are shared between taxpayers and gas users in Poland, Croatia and Greece, and exclusively assigned to gas consumers in France, the Netherlands or in Italy. Furthermore, in Italy, taxpayers bear exclusively the costs of gas storage filling while in Austria these are shared with gas consumers.

The observed uneven cost recovery approaches for gas security of supply measures might lead to possible distortions in competition between European gas consumers, as gas users in some countries (ex. Germany, Italy, Poland) will be not be charged (all) the cost of securing gas supplies, and in others they will have to pay all these costs through their gas bills.

Figure 4: Benchmark of the measures by party bearing the final costs

Source: FTI Consulting analysis

Greek government tasked DESFA to install an FSU at the Revithoussa LNG terminal

Measure: At the request of the Greek government, the Greek natural gas transmission system operator DESFA chartered a floating LNG storage unit, with the capacity of 145,000m3, located 700m offshore the Revithoussa LNG import terminal. The entry into operation of the FSU was marked by the unloading of the first cargo at the end of August 2022. Thanks to the FSU, the total national LNG storage capacity increased by 64%, i.e. from 225,000m3 to 370,000m3 LNG.

Costs: Expected annual cost for a one-year lease excluding operating costs (OPEX) is 20 million EUR.

Cost recovery mechanism:

- Cost of lease: Paid through the Security of Supply account, which is recovered from a security of supply levy set by regulator and applied to all gas users by retailers, with different rates according to different types and consumptions.

- OPEX: Borne by LNG terminal users (and partly transmission users, as there is a cost sharing of all Revithoussa LNG costs to transmission users from pre-existing regulation). OPEX are significant as the FSU cannot handle the Boil-Off Gas.

- External funding: DESFA plans to apply for funding under the REPowerEU Plan chapter of the Recovery and Resilience Plans for the future acquisition of the FSU.

Duration: The FSU has been chartered by DESFA for the period of 12 months extendable to additional six months.

Filling in of gas storages in Germany has been funded by a neutrality charge levied at gas exit points

Measure: On 29 July 2022, the German government approved a methodology for the design of a neutrality charge enabling the filling of gas storage by the market area manager, Trading Hub Europe (THE), which is required to pay for the storage service to traders and to access 20% of the stored quantity.

THE is entitled to use a combination of gas storage mechanisms: a provision mechanism for the use of unused storage capacity (if not filled by market participants), and the tendering of strategic- based options for the market-based filling of storage capacity:

- In stage 1, the storage facilities are filled in by using market-based activity accompanied by tenders of the so-called Strategic Storage-Based Options (SSBOs) by THE;

- In stages 2 and 3, the market area manager can undertake further tenders of SSBOs to make up for any difference between the required and actual storage levels;

- If neither stage is sufficient, THE is responsible for gas procurement and its injection into storage.

Costs: Expected cost for the measure is 34 billion EUR.

Cost recovery mechanism:

Costs incurred by the market area manager to ensure the security of supply are financed by a neutrality charge imposed on entities responsible for network balancing for volumes physically withdrawn daily at cross-border interconnection points and virtual interconnection points. The neutrality charge is split as (i) a registered power metering (RLM) neutrality charge (3.90 EUR/MWh) for hourly-metered customers and (ii) a standard load profile (SLP) balancing neutrality charge (5.70 EUR/MWh) for standard load profile customers, borne by balancing group managers serving RLM and SLP exit points

Duration: The measure is expected to remain in force until March 31, 2024.

Annex: Objective & Approach

The objective of this study was to identify measures assigned by governments to gas companies, analyse them and conduct a benchmark of identified measures across the four aforementioned analytical dimensions in order to determine the new roles and their nature (total costs, cost recovery method, duration) assigned to TSO and gas market players, as a consequence of the energy crisis.

Our approach to conduct this study was threefold: Firstly, we carried out systematic research of gas-related security of supply measures implemented across the main European markets. Secondly, based on the identified measures, we researched relevant legislative and regulatory texts to confirm that it was a public authorities’ decision that appointed a market player to implement a certain measure, as well as to identify and analyse the set of key analytical dimensions relevant to each measure – measure description (target and means to improve security of supply), measure category (measures related to gas volumes, infrastructure capacities and other measures), entity in charge of measure’s implementation (TSOs or other entities), costs and costs coverage (final bearer of costs – gas consumer, tax payer or both) and duration (short, medium and long-term measures). Thirdly, the research was complemented by interviews with several European TSOs and other gas market players.

Endnotes:

1: We considered government-mandated measures as (1) gas security of supply measures supported by a piece of legislation or regulation obliging a given entity to implement the given measure, and (2) gas security of supply measures implemented by state-owned (in part of in full) gas companies of systemic relevance.

2: This excludes capacities added by private companies not subject to government mandate. The regasification capacity of one of the FSRUs chartered in Italy is unknown and therefore not reflected in the figure.

3: Solidarity mechanism for the security of gas supply: Development of a solidarity platform enabling potential targeted curtailments of gas consumption to supply prioritized areas/consumers.

4: Total expected budget of 6.56 billion EUR for five FSRUs totalling to the capacity of ~31 bcm/year. Source: Euroactiv, German Federal Ministry for Economic Affairs and Climate Action

5: Total regasification capacity addition of 20.6 bcm through four FSRUs, with the total costs of 700 mEUR. The capacity increase at the Revithoussa LNG is not taken into account, as the associated costs are unknown.

6: Greece: The Revithoussa LNG terminal expansion has been excluded as associated development costs are unknown. Italy: Regasification capacity for the Portovesme FSRU is unknown therefore the associated costs are not reflected in the calculation. Spain: LNG terminal of El Musel has been excluded due to the low reliability of the expected costs. France is not included in the list as the costs for acquisition of the FSRU are unknown. Poland: It is not included in the calculations, as the associated costs with the capacity increase at Gdansk FSRU are unknown.

Published

abril 20, 2023

Key Contacts

Key Contacts

Senior Managing Director