Antitrust Rewired: The Growing Need for Vigilance in Private Equity

-

October 03, 2024

Downloads Download Article

Download Article

-

Until recently, antitrust was a topic private equity (“PE”) firms could comfortably avoid. In fact, when PE firms encountered antitrust regulators, it was often in the role of a rescuer — swooping in to rescue merger deals by carving out spin-offs that required divestiture to alleviate any concerns about potential anticompetitive effects.1

PE investments also created other positive spillover effects in an industry, which were then absorbed by other companies operating in the same space. But that unfettered deal-making era is over. In the last few years antitrust regulators have turned their aim toward PE firms with several different impactful regulatory changes, making it essential that partners and general counsel at PE firms include quantitative antitrust due diligence in their deal-making toolkit.

A New Era of Antitrust Enforcement

At least three major developments in the antitrust regulatory space could directly impact PE companies. First, in June 2023, the Federal Trade Commission (“FTC”) proposed major changes to the Hart-Scott- Rodino (“HSR”) pre-merger filing requirements.2 Many of these changes are aimed at catching previously undetected deals, especially serial-acquisition deals by the PE firms. If these proposed changes are adopted,3 PE firms will have much more extensive disclosure requirements, including information about their investment structures, past investments in the same industry and other portfolio companies, even if they are not directly involved in the deal under scrutiny.4

Second, toward the end of 2023, the FTC took its first enforcement action in 40 years on an issue frequently faced by PE firms: interlocking directorates. In the case of PE firm Quantum Energy Partners’ acquisition of EQT Corporation, both direct competitors in the Appalachian Basin’s natural gas market, the FTC imposed several structural remedies to prevent potential competitive harm.5 Quantum Energy Partners was prohibited from holding a seat on EQT’s Board, required to divest its EQT shares, barred from exchanging anticompetitive information with EQT, and mandated to unwind an existing joint venture between the two companies.6

Finally, at the end of 2023, the Department of Justice (“DOJ”) and the FTC released their new and expanded Merger Guidelines with a new focus on minority ownership and partial acquisitions, an area of special concern for PE firms.7 The guidelines note that even nonvoting interests or minority stakes can impact competitive decision-making and influence a firm’s competitive strategies.8

The Spotlight on Private Equity

In addition to these changes, the agencies have explicitly identified two industries in which PE firms have been particularly active: healthcare9 and real estate.10

Healthcare Industry

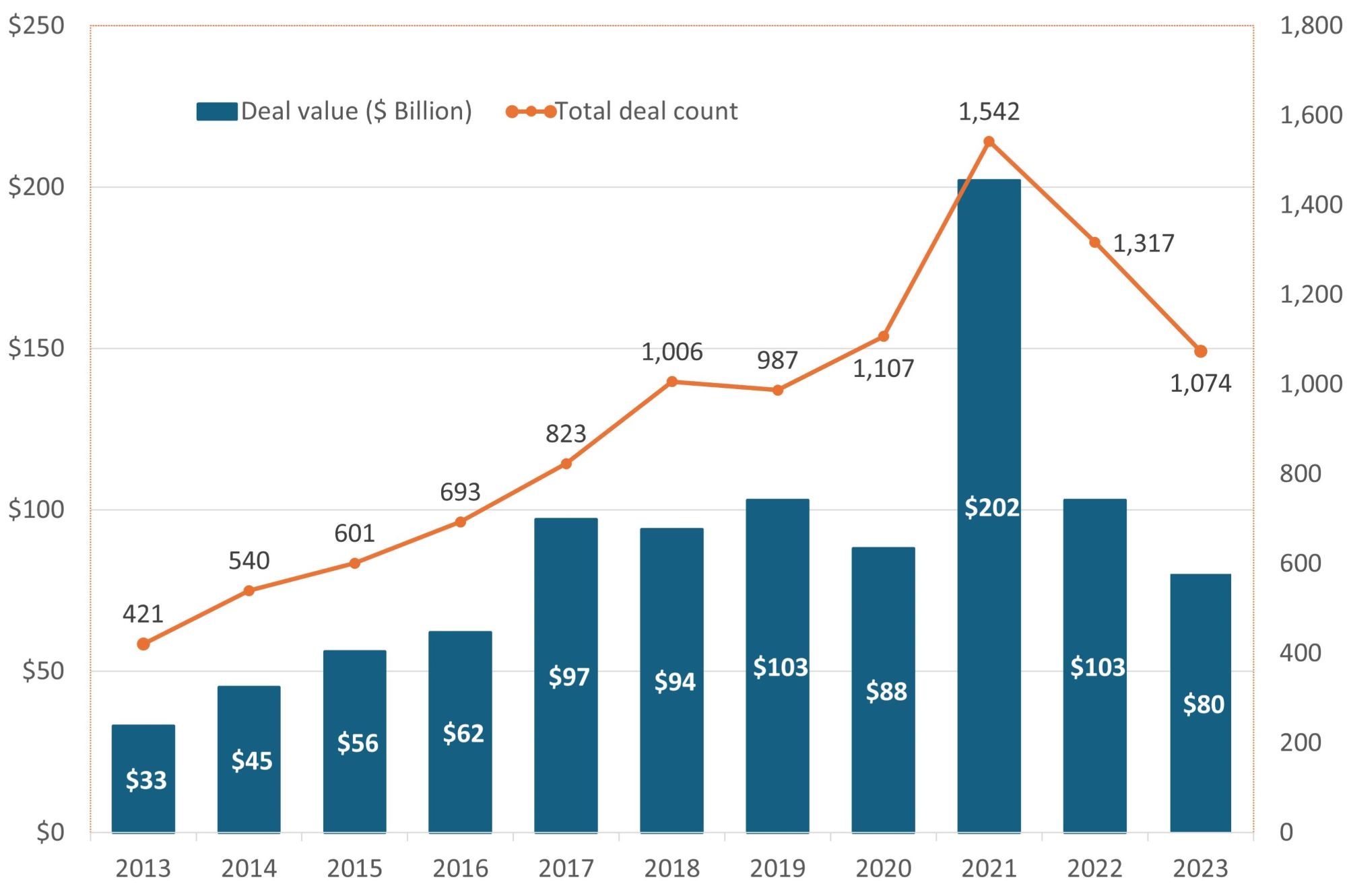

The healthcare industry has seen a surge in private equity deals since 2013, with the number of transactions increasing by 2.5 times and peaking in 2021. During this same period, the total value of these deals increased more than fivefold, highlighting a robust growth trend in the healthcare investment landscape.

Chart 2: PE Investment in Healthcare from 2013 until 2023.11

Source: American Health Law Association “Private Equity in the Cross Hairs: Navigating Increasing Antitrust Scrutiny of Private Equity Deals in Health Care” On-Demand Webinar, May 22, 2024.12

This PE investment boom in the healthcare sector has attracted considerable attention from regulatory bodies at both the state and federal levels in recent years. Agencies have flagged the healthcare industry as an area of concern, claiming that PE firms’ involvement in healthcare directly results in poorer health outcomes, staffing issues and higher overall healthcare costs. The agencies have concerns about the PE firms’ goals of maximizing profits while potentially trading off the quality of care provided to patients.13 Robust research on this phenomenon is still nascent and inconclusive, prompting the agencies to call for further investigation and research into the impact of PE on healthcare.14

Three distinct avenues pursued by the agencies illustrate this heightened scrutiny specifically for healthcare providers. First, the DOJ, FTC, and Health and Human Services (“HHS”) jointly released a Request for Information (“RFI”) to seek public comments on the effects of PE acquisitions involving healthcare providers.15 Second, the FTC held a virtual workshop to highlight the two types of transactions they find most problematic: “strip-and-flip” transactions wherein PE firms strip the most valuable assets first and sell them before selling the left over company to generate quick returns; and “roll-up” transactions that use of a series of smaller transactions not subject to antitrust review while consolidating market share.16 “Roll-up” transactions (i.e., serial acquisitions) were also specifically called out as an area of potential competitive concern in the new merger guidelines released at the end of 2023.17 Third, the three agencies collaboratively launched the HealthyCompetition.gov website, designed for public reporting of potentially unfair and anticompetitive practices happening in the healthcare industry.

And this focus extended into direct enforcement action. Last year, the FTC sued PE firm Welsh Carson for its involvement in a series of acquisitions of anesthesia services in Texas, alleging monopolization of this market.18 The Court eventually dismissed the FTC’s claims. However, the agencies made it clear this was an opening salvo in what will become increasing scrutiny of healthcare investments by the PE firms.19

Real Estate Industry

The real estate sector, particularly the rental market, is another industry experiencing significant recent PE acquisition activity. As of June 2022, approximately 1

out of 60 rental homes in the US were owned by private equity companies.20 The numbers are similarly high

for apartment rentals and manufactured-home site rentals.21 The DOJ and FTC are intensively exploring the implications of technological advancements in the real estate rental sector, with a specific focus on algorithmic price setting.22

Algorithmic price setting, also known as dynamic or surge pricing, is a flexible and automated system of price determination to achieve a given business goal. For example, an Uber ride at 9pm on a rainy night costs higher than a sunny daytime ride for the same destination. To achieve this level of dynamic price optimization, companies must collect a lot of data on their customers, competitors, local and global events and trends, social media, news, and the weather among other things. Then they put these data through predictive algorithms to analyze the impact of various variables on demand and prices.

Algorithmic pricing is both a cutting-edge competitive advantage and a potential antitrust risk, depending on whose data the algorithms are using and how. When competitors in real estate rentals share their confidential data with an intermediary company that algorithmically proposes optimal rental prices based on the collective dataset, agencies grow concerned. Antitrust agencies have been often submitting Statements of Interest to articulate their stance on these issues.23 “Whether firms effectuate a price-fixing scheme through a software algorithm or through human-to-human interaction should be of no legal significance,” the FTC and DOJ noted recently. “Automating an anticompetitive scheme does not make it less anticompetitive.”24 Private equity firms acquiring companies that use algorithms to determine its rental prices could be acquiring unexpected and large antitrust liabilities.

Shifting Antitrust Risk Calculations for PE Firms

This recent increased focus on private equity financed deals changes the antitrust risk calculation for PE firms and creates a more urgent need for PE firms to be more proactive in antitrust monitoring of their transactions in anticipation of agency or private scrutiny. The best way to minimize antitrust scrutiny is for a PE deal partner to adopt a forward thinking approach. PE firms may then be able to develop a deal structure that diminishes anticompetitive concerns.

With this vigilance in mind, PE firms would do well to use a 3-step antitrust risk minimization method:

- Channel your inner antitrust economist: Conduct a quantitative assessment of the relevant market, market concentration, and acquisition target’s market share.

- Dive deep into competitive effects: Analyze the potential competitive effects of an acquisition beyond just concentration concerns. Examine whether the deal will import any low-visibility but high-cost antitrust problems like algorithmic price fixing.

- Craft a deal that sidesteps antitrust pitfalls: Use the insights gained from the first two steps to structure the deal in a way that minimizes antitrust risks. For example, in the case of a serial acquisition, a deal partner could take a holistic view of a market, and after going through the first 2 steps, identify acquisition targets that do not significantly increase market concentration levels and that avoid anticompetitive effects while potentially carrying similar profit potentials.

Footnotes:

1: Federal Trade Commission, “FTC Requires Albertsons and Safeway to Sell 168 Stores as a Condition of Merger,” FTC Press Release, (Jan 27, 2015).

2: Federal Trade Commission, “Premerger notification; Reporting and waiting period requirements: Notice of proposed rulemaking,” Federal Register, 88(42178), (2023).

3: “During the American Bar Association Antitrust Spring Meeting held from April 10–12, 2024, top officials from the FTC and the DOJ Antitrust Division previewed that they expect final changes to the HSR premerger notification form to be finalized soon.” Sidley, “Sidley Perspectives on M&A and Corporate Governance,”(June 2024), pg. 21.

4: Federal Trade Commission, “FTC and DOJ Propose Changes to HSR Form for More Effective, Efficient Merger Review,” FTC Press Release, (June 27, 2023).

5: Federal Trade Commission, “FTC Acts to Prevent Interlocking Directorate Arrangement, Anticompetitive Information Exchange in EQT, Quantum Energy Deal,” FTC Press Release, (August 16, 2023).

6: Federal Trade Commission, “FTC Acts to Prevent Interlocking Directorate Arrangement, Anticompetitive Information Exchange in EQT, Quantum Energy Deal,” FTC Press Release, (August 16, 2023).

7: Department of Justice and Federal Trade Commission, “Merger Guidelines,”(Dec 18, 2023).

8: Department of Justice and Federal Trade Commission, “Merger Guidelines,”(Dec 18, 2023), pg. 28.

9: Federal Trade Commission, “Private Capital, Public Impact: An FTC Workshop on Private Equity in Health Care,” FTC Workshop, (Mar 5, 2024).

10: Hannah Garden-Monheit and Ken Merber, “Price fixing by algorithm is still price fixing,” FTC Business Blog, (Mar 1, 2024).

11: 2023 deal count is an estimate by authors of the webinar hosted by the American Health Law Association.

12: Herbert Allen, Emily Walden, and Bryn Williams, “Private Equity in the Cross Hairs: Navigating Increasing Antitrust Scrutiny of Private Equity Deals in Health Care,” American Health Law Association Education Center On-Demand Webinar, (May 22, 2024).

13: Federal Trade Commission, “Federal Trade Commission, the Department of Justice and the Department of Health and Human Services Launch Cross-Government Inquiry on Impact of Corporate Greed in Health Care”, (March 5, 2024).

14: Federal Trade Commission, “FTC and DOJ Seek Info on Serial Acquisitions, Roll-Up Strategies Across U.S. Economy”, (May 23, 2024).

15: Department of Justice, Department of Health and Human Services, and Federal Trade Commission, “Request for Information on Consolidation in Health Care Markets,” (Mar 4, 2024), pg. 3.

16: Federal Trade Commission, “Private Capital, Public Impact: An FTC Workshop on Private Equity in Health Care,” (Mar 5, 2024).

17: Department of Justice and Federal Trade Commission, “Merger Guidelines,”(Dec 18, 2023).

18: FTC Press Release, “FTC Challenges Private Equity Firm’s Scheme to Suppress Competition in Anesthesiology Practices Across Texas,” (Sept 21, 2023).

19: Federal Trade Commission, “FTC and DOJ Seek Info on Serial Acquisitions, Roll-Up Strategies Across U.S. Economy”, (May 23, 2024).

20: Americans for Financial Reform, “Estimate of Private Equity Ownership of Housing Units,” AFR Research Memorandum, (Jun 28, 2022), pg. 2.

21: Americans for Financial Reform, “Estimate of Private Equity Ownership of Housing Units,” AFR Research Memorandum, (Jun 28, 2022), pg. 3-4.

22: Hannah Garden-Monheit and Ken Merber, “Price fixing by algorithm is still price fixing,” FTC Business Blog, (Mar 1, 2024)

23: Federal Trade Commission, “Statement of Interest of the United States of America,” McKenna Duffy v. Yardi Systems, Inc., et al., (Mar 1, 2024).

24: Federal Trade Commission, “Statement of Interest of the United States of America,” Karen Cornish-Adebiyi, et al. v. Caesars Entertainment, Inc., et al., (Mar 28, 2024).

Published

October 03, 2024