Fair Lending and Responsible Banking Solutions Brochure

Consumer Financial Services

-

May 05, 2023

Downloads Download Brochure

Download Brochure

-

Inequity in the lending and financial markets continue to be a primary focus of regulators. In addition, communities will soon have more visibility of an institution’s small business lending practices. Whether it’s mortgages, small business, automotive or other consumer lending products, entities need to manage their fair lending risks related to pricing, underwriting, redlining, marketing, appraisal bias, among others.

FTI Consulting’s Consumer Financial Services (“CFS”) is composed of professionals with in-depth industry, regulatory and consulting experience providing practical fair lending compliance insights and support. FTI Consulting experts have significant experience assisting financial institutions of all sizes and complexity levels, often in response to critical fast moving regulatory matters.

Product Based Risks

Small Business Lending

Section 1071 of the Dodd-Frank Act amended the Equal Credit Opportunity Act (“ECOA”)1 requiring significant operational changes in the collection, monitoring and reporting of credit and applicant demographic information of small business lending. Small business lenders should not only begin implementing the requirements but should also start reviewing, as early as practical, their newly acquired data to assess fair lending risks in preparation for regulatory examinations.

FTI Consulting has the expertise to provide a full solution to assist small business lenders with assessing their operational risks, implementing the requirements of the 1071 Rule and identifying any fair lending risks based on the newly gathered data.

Mortgage Lending

Regulators continue to focus on fair lending risk in the mortgage marketplace. Mortgage lenders incur risk throughout the mortgage product life cycle, from gathering the required data under the Home Mortgage Disclosures Act2 to assessing fair lending risk in origination and servicing activities. Such risks include pricing, underwriting, redlining, digital marketing, appraisal bias and loss mitigation activities. FTI Consulting experts apply their regulatory and business experience to prepare clients for their next regulatory examination or assist with responses to examination findings and enforcement actions.

Consumer Lending

Consumer credit products (e.g., automotive, unsecured, or credit cards) each have unique lending risks which require diligent mitigation controls. Further, unlike mortgage or small business lending, lenders offering consumer products are unable to collect applicant demographic information for further fair lending analysis. FTI Consulting understands these complexities in assessing fair lending risk. Our CFS professionals and dedicated Data Analytics teams have extensive experience developing strategic business solutions requiring in-depth analysis of large sets of financial, operational and transactional data. Such analysis includes applying Bayesian Improved Surname Geocoding (“BISG”) which employs the applicant’s name and address to proxy for the applicant’s ethnicity/race and gender.

FTI Consulting has unrestrained capabilities to analyze varying data despite the product type, size or complexity of the lending operations of financial institutions.

Fair Lending Regulatory Solutions

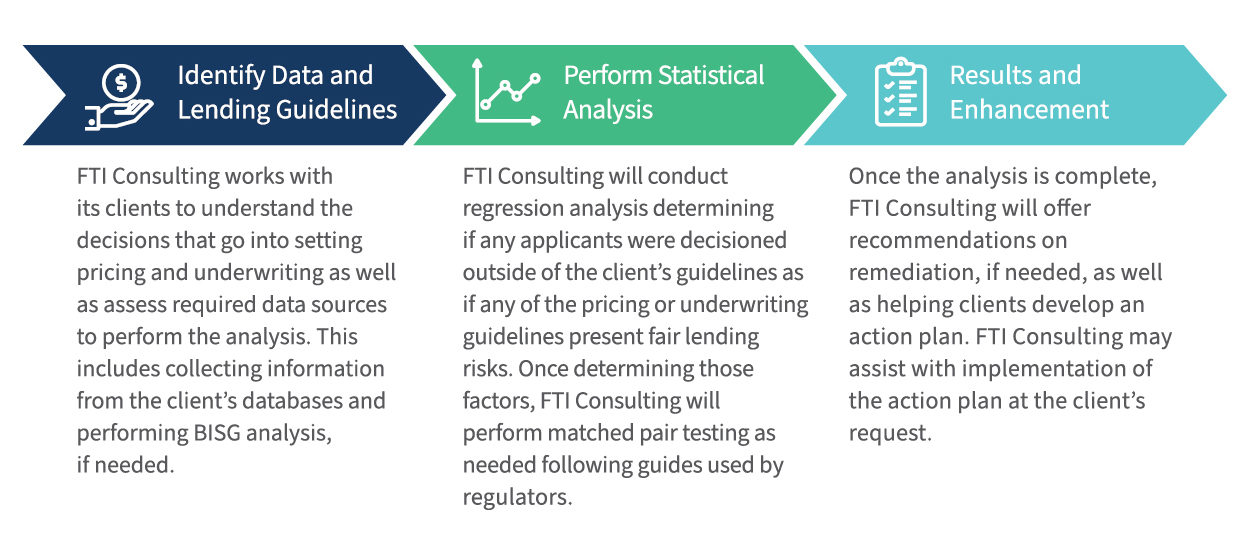

Pricing and Underwriting

FTI Consulting uses a proven methodology when performing pricing and underwriting reviews to determine possible fair lending risks.

Artificial Intelligence and Machine Learning (“AI/ML”) Modeling

Models that use AI/ML are replacing traditional credit and marketing decisions. As these technologies advance, lenders must be conscious of how their models perform. Regulators have expressed concerns around these models, or “Black Boxes”, and have stated that lenders must have adequate controls to reduce fair lending risks. FTI Consulting’s CFS and Data and Analytics teams understand the complexity of these models and have the expertise to assist lenders in establishing model governance which includes fair lending analysis of the model.

Redlining

FTI Consulting can assist in analyzing application generation against peer institutions using publicly available data (e.g., HMDA data) and/or FTI Consulting’s industry benchmarks. Additionally, FTI Consulting will review marketing practices (digital and non-digital), branch distribution and other activities (e.g., internal communications) to help identify potential fair lending risks.

1071 Small Business Lending Rule (“1071 Rule”)

The new 1071 Rule has created heightened regulatory focus on inequity in small business lending and small business lenders should expect scrutiny regarding their lending operations and access to credit for small and minority-owned businesses.

FTI Consulting has the expertise to help lenders implement the rule requirements as well as identify fair lending risks using the newly collected data points. The new rule certainly poses operational challenges for small business lenders. In addition to collecting information from small business applicants, lenders must have a keen eye in evaluating their policies, procedures and practices throughout the lifecycle of the application to ensure compliance with the 1071 Rule.

FTI Consulting experts can assist with implementation, testing and evaluation of compliance with the new data collection and reporting requirements, as well as assessment in accordance with the institution’s fair lending program.

CMS Update

The first phase in implementing the new rule requirements is to ensure the client’s Compliance Management System is updated to conduct the regulatory requirements and mitigate the risk involved. This includes updating P&P,

training, and monitoring and audit schedules.

Implement and Test

After establishing the controls necessary, the client needs to implement the rule requirements and immediately test the implementation to ensure all required data is collected.

Fair Lending Analysis

While the initial concentration from regulators will be on rule

implementation, lenders should not wait to start assessing for fair lending

risks using the new data. Such risks include pricing, underwriting and redlining.

Remediate

Should the lender identify disparities, they should quickly develop an action

plan and make all necessary actions to remediate applicants.

CMS Update

Financial Institutions should determine that their Compliance Management System (“CMS”) is updated to identify new regulatory requirements and mitigate the risk involved. This includes updating P&P, training, monitoring and audit schedules.

Implement and Test

After establishing the necessary controls, financial institutions need to implement the rule requirements and immediately test during and after implementation to ensure all required data is collected and can be transmitted accurately.

Fair Lending Analysis

While the initial focus from regulators will be on rule implementation, lenders should not wait to start assessing for fair lending risks using the new data. Such risks include pricing, underwriting and redlining.

Remediate

Should lenders identify disparities, they will need to quickly review for root cause, develop an action plan and take necessary actions to remediate practices and provide redress for applicants as appropriate. Policies and procedures may require adjustment to mitigate small business fair lending risk going forward.

Appraisal Bias

Appraisal Bias examinations and enforcement are novel to the mortgage industry. Regulators are expanding their reviews to include possible discrimination in appraisals. FTI Consulting has a readily available systemic solution to support clients in identifying potential fair lending risks. FTI Consulting’s solution includes:

Derogatory Terms

- Performs a keyword search and builds adaptive learning to identify terms not previously considered

Reconsideration of Value

- Performs a review of the entity’s reconsideration of value process

Valuation Differences

- Uses statistical significance tests to compare valuation results against initial sales price or estimated value

- Identifies if any correlation exists between valuation differences and a prohibited basis

Case Study: Discriminatory Lending Practices

Situation

A federal regulator made allegations regarding unfair, deceptive and discriminatory lending practices for a large financial institution. The allegations involved the institution’s use of background checks in the lending process and whether the practice resulted in discrimination against racial minorities and specific geographic neighborhoods.

Our Role

FTI Consulting provided economic and statistical analysis of the discriminatory allegations. The assessment included the lending program’s geographic differences and correlations with racial minorities. Additionally, FTI Consulting assisted the client and counsel with process improvements and procedures to ensure that lending processes were not leading to potentially discriminatory outcomes for protected classes.

Our Impact

FTI Consulting’s analysis allowed the client to demonstrate their lending practices were not discriminatory and implement process improvements for on-going compliance. Further, FTI Consulting’s analysis allowed the institution to address reputation risks and provide on-going metrics to senior management regarding the lending program’s effectiveness with respect to protected classes.

Case Study: AI/ML Model Bias Review for UDAAP and Fair Lending

Situation

A large digital marketing company that offers advertising, marketing, transaction solutions, customer data and cross-channel campaign management requested assistance in analyzing their models for fair lending risk. FTI Consulting performed regression analysis to review their proprietary predictive AI/ML models and supporting data for risks related to ECOA, FHA and UDAAP.

Our Role

FTI Consulting performed analysis for all data attributes and identified “red-flags” that could be problematic from a fair lending and UDAAP perspective. Further, FTI Consulting used statistically sound analysis to review use cases, features, model logic and output to determine possible disparate impact and regulatory risk. Where appropriate, data was compared and contrasted regarding loan decisioning and pricing for protected classes and/or majority-minority census tracts.

Our Impact

FTI Consulting’s professionals identified various risks within the models and campaign management programs and recommended controls to meet regulatory expectations. FTI Consulting assisted the client in creating model risk management documentation which was made available to the client’s financial institution partners and to demonstrate compliance to regulators.

Related Insights

Related Information

Published

May 05, 2023

Key Contacts

Key Contacts

Senior Managing Director

Senior Managing Director

Senior Managing Director

Managing Director