ESG: A New Value Creation Lever for IROs and CFOs

-

avril 24, 2024

-

Introduction

Environmental, social and governance (“ESG”) has long been associated with doing good. From its origins in corporate social responsibility to the current sustainability reporting regime, one could easily mistake ESG as yet another mechanism to encourage companies to take more responsibility for the environment and society at large. At the extreme, this altruistic view of ESG has been challenged and weaponized in the current political environment. While this politicization of ESG makes for good theater, it overshadows the value creation potential that can be driven by a well-run sustainability program. Bear in mind, ESG is just a tool, a corporate Swiss Army knife of sorts. It can be used in a multitude of capacities with varying levels of impact both within and outside of the company wielding it. However, many companies are not yet fully harnessing their ESG programs to create tangible financial value.

It’s therefore understandable that many investor relations officers (“IROs”) and CFOs have kept themselves at arm’s length when it comes to their companies’ ESG programs. This attitude must change as we enter the new sustainability reporting regime. As disclosures become more standardized, driven by a shift to mandatory reporting, the market will also shift in how it evaluates ESG programs. Investors will no longer credit companies for simply providing a comprehensive set of sustainability disclosures, but will instead focus on the actual performance of such disclosures relative to peers and the broader market. The train is leaving the proverbial station and IROs and CFOs must decide if they’re getting on board.

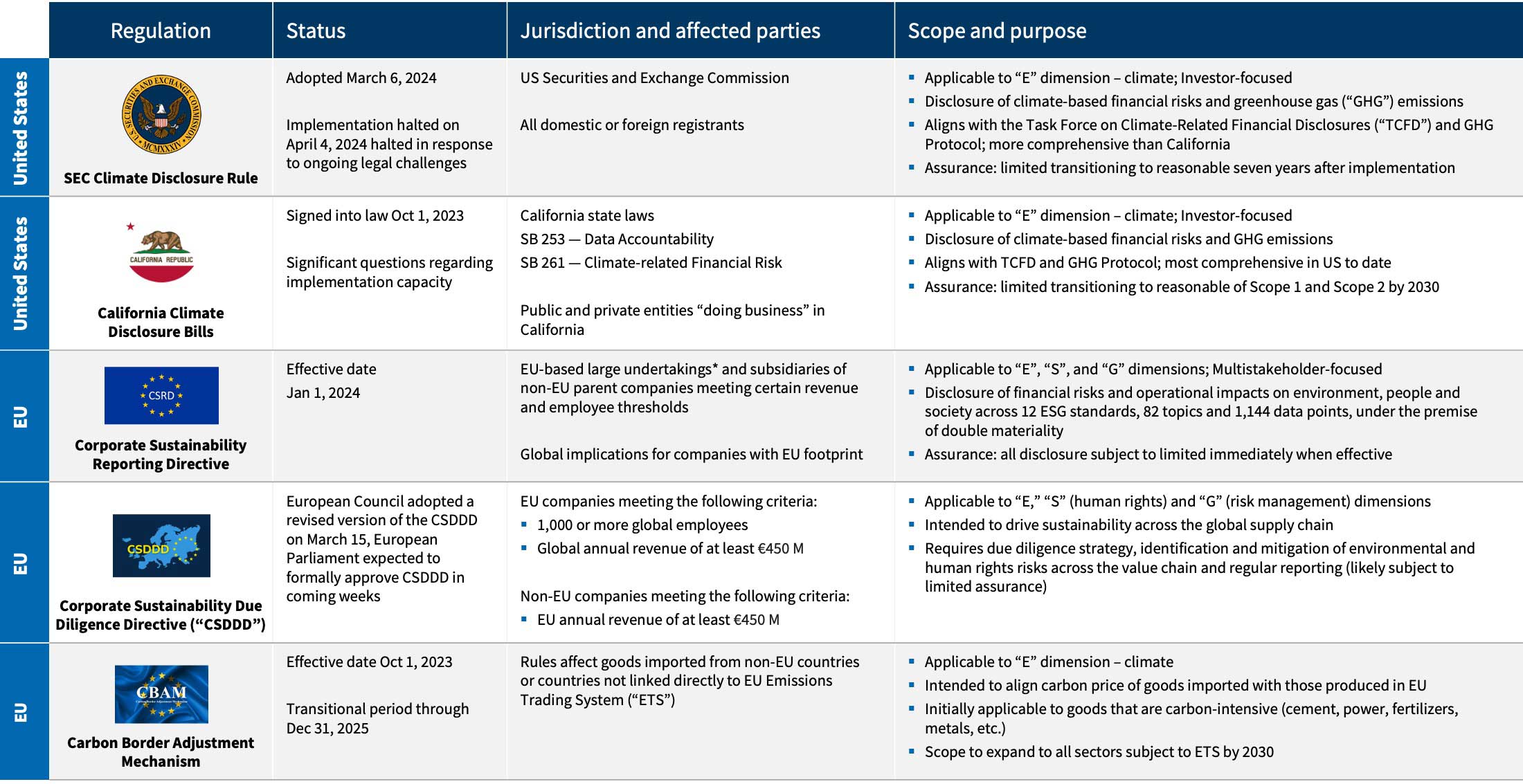

The New Reporting Regime

New sustainability regulations (see figure below) are largely aligned with more established yet voluntary frameworks, such as the Task Force on Climate-Related Financial Disclosures (“TCFD”) and the World Resources Institute’s Greenhouse Gas Protocol. But they vary in many respects, including assurance mandates, implementation deadlines and explicit non-compliance penalties. In turn, compliance will require unprecedented internal collaboration, including among the investor relations function and the office of the CFO.

* Large undertakings include companies that exceed at least two of the following thresholds as of the end of the last two consecutive financial years: 1) Total assets exceeding €25 million; 2) Net turnover exceeding €50 million; 3) An average number of employees exceeding 250.

Compliance with these new regulations will become table stakes over the next few years, similar to financial reporting today. However, the responsibility for understanding and disclosing drivers of performance, as well as related engagement with shareholders, will undoubtedly fall on IROs and CFOs. As ESG and financial reporting increasingly merge, these corporate leaders will need to improve their game to manage and understand such complex matters.

To help IROs and CFOs focus on what matters most, we’ve outlined four levers worth considering to augment investor relations programs and ensure value creation in this evolving, regulation-centered environment.

Value Creation Levers

Enhancing Climate-Literacy

At a minimum, IROs and CFOs must deepen their familiarity with relevant climate-related risks and transition scenarios. This is necessary to speak intelligently on potential financial impacts under various timeframes and climate scenarios, as well as any investments necessary to decarbonize. While targeted education will be helpful, learning will come from action, gaining exposure to risk assessments and internalizing how these risks may impact underlying business performance. To this end, we recommend active participation in evaluating the financial impacts of climate change and managing related risks and potential mitigants.

Optimizing the Approach to Controversies

Controversies identified by ESG rating agencies are growing in importance, impact and scrutiny. Reputational risks will remain front and center, covering a wide range of incidents and issues, from a plant explosion to a health and safety concern or environmental contamination. Additionally, ESG rating downgrades and subsequent re-weightings will surely continue to take place within corresponding indices. Heightened risk in capital markets is likely, as ESG investment policies among institutional investors continue to formalize. These investment policies are frequently informed by and aligned with global norms as defined by the United Nations Global Compact (“UNGC”) and the Organisation for Economic Co-operation and Development (“OECD”). In practice, a controversy flagged by a rating agency deemed severe and/or structural will almost certainly violate such norms, resulting in the potential divestment of a company if the underlying risks — and management — are not addressed in a timely fashion.

Controversies may also affect the screening process run by asset managers to identify new investment opportunities. This is particularly true for investors with funds (Article 6, 8 and 9) that are subject to the EU’s Sustainable Finance Disclosure Regulation (“SFDR”). Given the potential impact to available capital and fund flows, IROs and CFOs should enhance their crisis plans to ensure potential controversies can be adequately managed.

Engaging with Stewardship Teams in the Offseason

Offseason engagement with the stewardship and governance teams of a company’s largest shareholders is another important risk mitigation step and a low-hanging fruit for IROs and CFOs. While stewardship teams are accustomed to corporate engagement when there is a proxy fight or shareholder proposal, few companies become involved at other times. Much like insurance, the payoff will not be immediate, but it is essential for companies to build relationships with these teams, demonstrate transparency and gain insight into shareholder expectations. At a minimum, companies will gain favor with proxy advisory firms that seek evidence of ongoing shareholder engagement. More importantly, these relationships and a track record of engagement will become invaluable to a company in a contested situation.

Institutional Shareholder Services recently noted that the number of shareholder proposals has increased every year for the past three years, largely driven by environmental and social proposals.1 Much like the overall shift from disclosure-based to performance-based evaluations of ESG programs, the content and focus of shareholder proposals will follow suit. Because of this, IROs and CFOs should be prepared to address material ESG issues and their underlying performance, implementing governance mechanisms to drive improvements where needed.

Pursuing Untapped Sources of Capital

In the current economic and interest rate environment, investors have become more risk averse and competition for capital is as fierce as ever. The increasing fund flows in this landscape demand out-of-the-box thinking and tapping new sources of capital where available. Chief among these are ESG and sustainability funds. According to Bloomberg Intelligence, global ESG assets could exceed $40 trillion by 2030 — up from $30 trillion in 2022.2 With a plethora of ESG ratings and funds available, improving disclosures and performance can make a real difference. However, compliance alone isn’t enough to attract ESG-focused capital.

With the right approach, IROs and CFOs can tap into this pool of capital, much of which resides outside of the United States today. This journey begins by gaining a deep understanding of the EU’s SFDR. Per the SFDR, institutional investors are required to report mandatory and voluntary indicators that demonstrate their portfolios’ environmental and social impact. As a result, these institutions make investment decisions based on corporate disclosures informed by the SFDR. Ultimately, this allows EU asset managers to market ESG fund products with specific regulated labels (e.g., “Article 6,” “Article 8” and “Article 9”). At a minimum, IROs and CFOs should understand where their company best aligns with these labeled funds to target the most appropriate investors. Given the recent adoption of the SEC’s Names Rule, we believe it’s only a matter of time before the United States follows suit and regulates ESG and sustainable investment products similarly to the EU.3

Conclusion

The time is now for IROs and CFOs to become more involved in their ESG and sustainability programs. At a minimum, compliance with new regulations will force IROs and CFOs to gain a deep understanding of their company’s sustainability disclosures and related performance drivers. However, mitigating risk like ESG controversies will be key to protecting value, while tapping into new sources of capital will provide upside potential from higher fund flows. IROs and CFOs who get on board quickly and use their ESG programs strategically will have the best chance of successfully navigating the new regulatory reporting regime.

Footnotes:

1: Kathy Belyeu et al. “2024 United States Proxy Season Preview: Environmental & Social.” Institutional Shareholder Services. (April 2024).

2: Adeline Diab and Rahul Mahtani. “ESG AUM set to top $40 trillion by 2030, anchor capital markets.” Bloomberg Intelligence. (February 2024).

3: “SEC Adopts Rule Enhancements to Prevent Misleading or Deceptive Investment Fund Names.” U.S. Securities and Exchange Commission. (September 2023).

Date

avril 24, 2024