Who Needs Rate Cuts Anyway?

-

June 12, 2024

Downloads Download Article

Download Article

-

Financial markets entered this year with a head of steam, propelled by the belief that Fed rate cuts were coming soon — and often — in 2024. Reading between the lines of Fed Chair Powell’s remarks in December led credit markets to believe that five or six cuts of 25 bps to the Fed Funds Rate were on tap for the year beginning in March. No such scenario has materialized to date or will materialize in 2024, with most Fed watchers now expecting no more than two rate cuts, likely starting in September, as inflation has been sticky enough to give the Fed pause. “Higher for longer” already has become a tired slogan. Treasury rates have widened considerably this year, with the 10-year Treasury note yield moving 60 bps higher since year end, while the Secured Overnight Financing Rate (“SOFR”), the reference rate for most leveraged loans, has barely budged in months and hovers at 5.3%.1

Creeping anxiety and a growing chorus of cautionary comments from the economic and business punditry over huge federal budget deficits and soaring federal debt2 have been suggested as contributing factors to a recent weak Treasury auction and persistently high Treasury rates — which is the benchmark rate for corporate bond yields. None of these developments has stuck to the original script, but much like a Curb Your Enthusiasm episode, the players are improvising to save the scene.

As it turns out, financial markets have rallied fiercely to date even as interest rates remain lofty, and the Fed refuses to give markets the candy they crave. The S&P 500 has surged 11% to date following a blowout return of 24% in 2023,3 and all three U.S. major market indexes have touched record highs in 1H24 without an iota of help from the Fed. Moreover, the rally in the S&P 500 has occurred with virtually no change in 2024 consensus earnings expectations for the index in over a year, meaning the index’s appreciation consists entirely of an earnings multiple expansion — from 17x 2024 EPS just over a year ago to 22x 2024 EPS currently.4 But it is not just equity markets that are determined to rally despite an uncooperative interest rate environment and persistent economic and geopolitical uncertainties. Bitcoin recently reclaimed its previous all-time high and other cryptocurrencies have moved appreciably higher this year, including dubious meme coins. Precious metals have made new highs and some industrial metals have retested multi-year highs, with copper recently nearing $11,000 per metric ton for the first time. Heck, even meme stocks — an infamous reminder of stock market gamification and greed in 2021 — are having a second act following a cryptic post on X by Roaring Kitty. Apparently, Dumb Money is still hanging around the hoop, this time competing with some quant fund algorithms that can detect and front-run most retail traders on both ends of a meme stock trade. Home prices also remain near record highs in many major markets, even as mortgage rates top 7.0%. Let’s face it: this has been an Everything Rally in 1H24 without any rate relief; one can only wonder if the same outcome would have occurred had the Fed already caved to the “Easy Money Forever” crowd or whether these rallies would have been even more exaggerated with a couple of rate cuts in the books by now. Surely the Fed will be considering the potential impact of its policy actions to further stoke exuberant markets of all kinds as it ponders the path and timing for rate cuts and balance sheet reduction. After all, when the rock group KISS can sell its music catalog and brand rights for $300 million,5 it might be time to consider whether valuations have been pushed beyond reasonable limits.

Corporate credit markets can be giddy too, though not in ways as glaring as the dozens of tech stocks with multibillion dollar valuations and no earnings history that are trading at 10 or 15 times next year’s projected revenue. Credit spreads (over comparable Treasuries) are the relevant measure of perceived credit risk, and, by that measure, credit investors also are feeling intrepid these days. Last month we discussed how depressed levels of distressed debt and a low distressed debt ratio amid an environment of robust corporate restructuring and default activity arguably was evidence of leveraged credit market complacency. Narrowing credit spreads on leveraged debt in 1H24 also signal investor complacency and market imbalances, driven by huge demand for fixed-income returns coming from a variety of capital sources. Leveraged loan repricings in 1H24 often are shaving 50 bps off loans originated within the last 12-18 months, while some BB loan spreads are approaching the lowest threshold for leveraged loans.

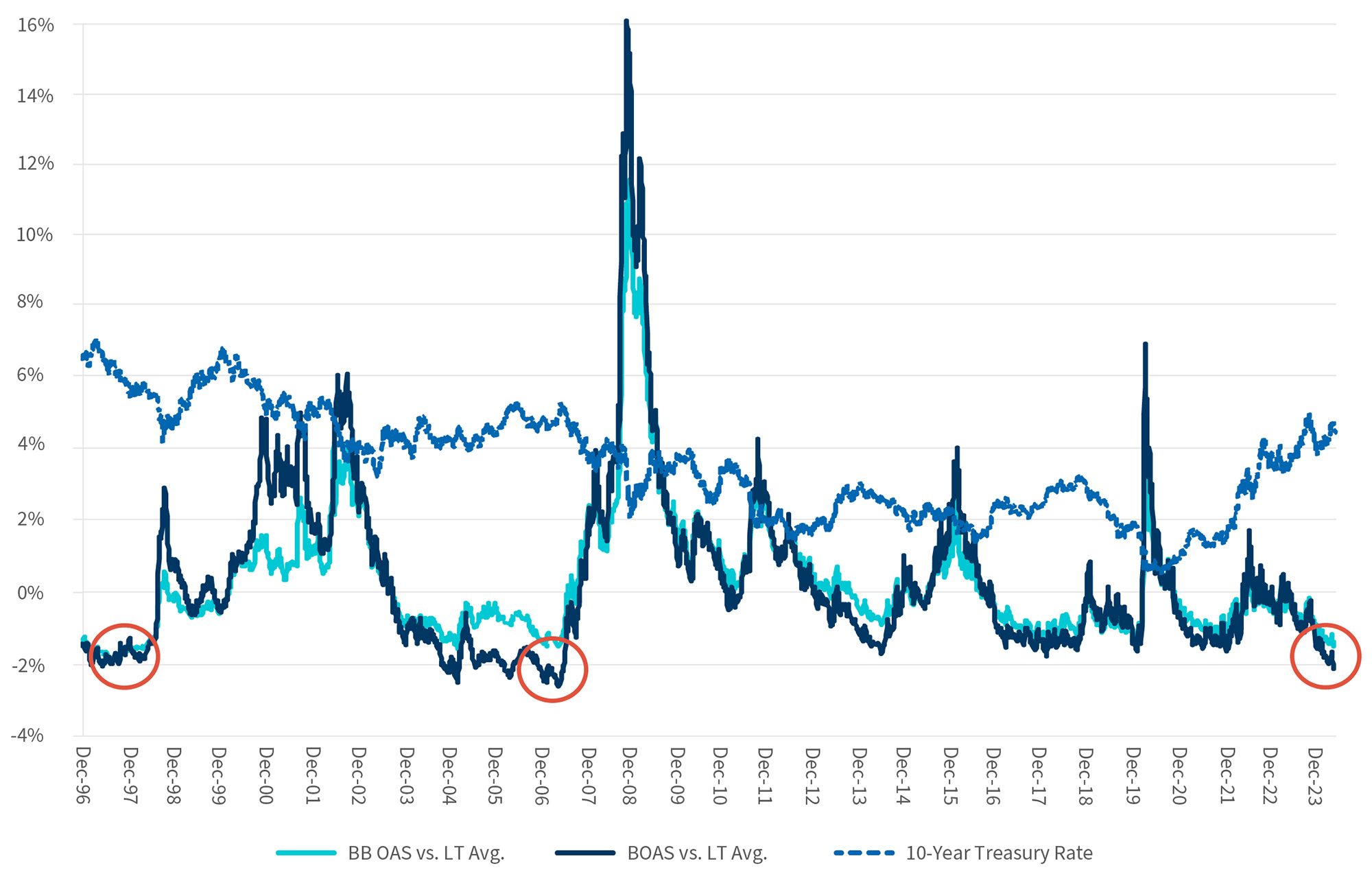

Figure 1: BB and B Rated Option-Adjusted Spreads Minus LT Average

Source: FRED, the Federal Reserve Bank of St. Louis

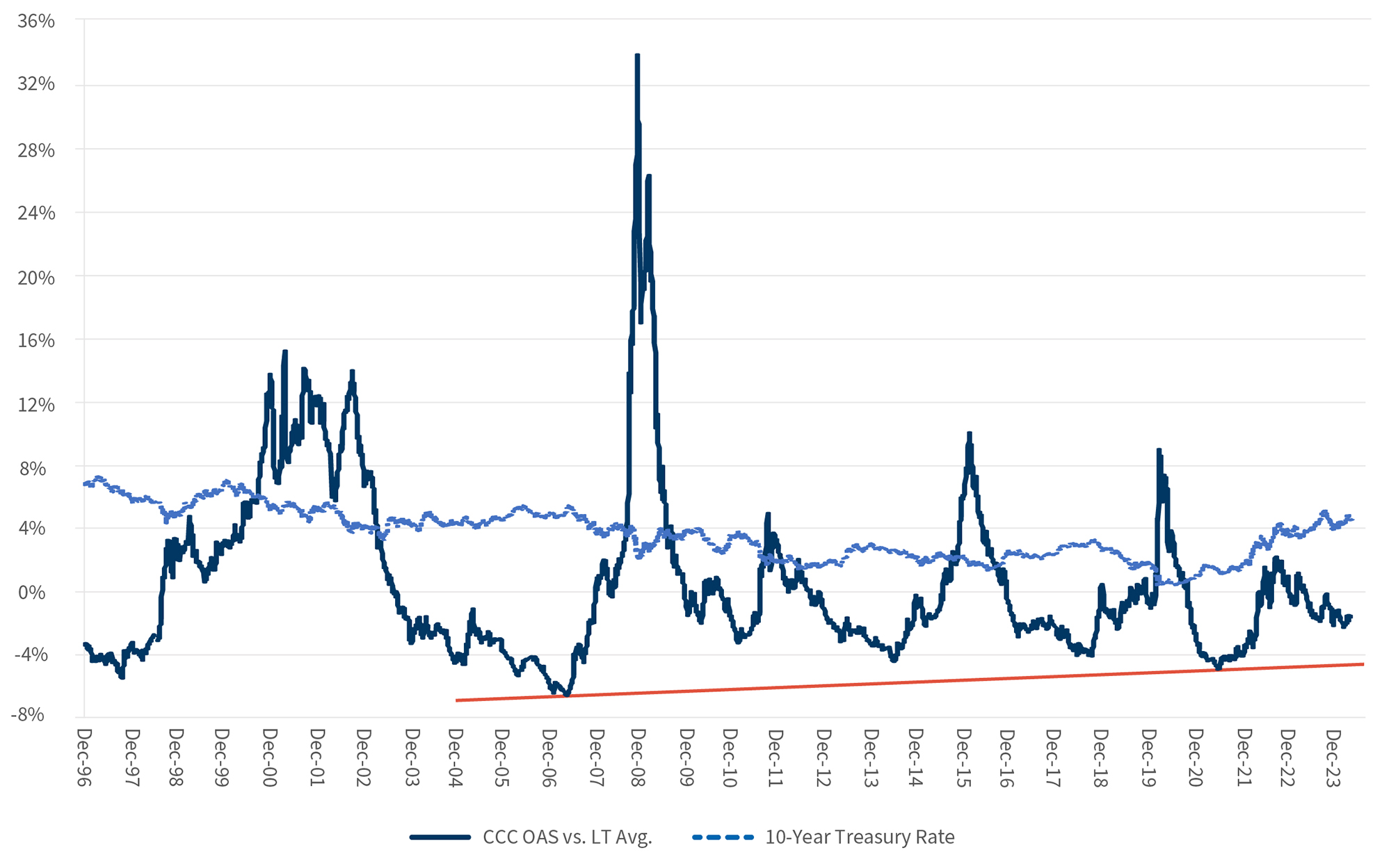

Credit spreads (“OAS”) on high-yield bonds have not only contracted this year but are at or near levels associated with historical periods that preceded severe market adversity. We evaluated historical credit spreads on bonds rated BB, B and CCC minus their respective long-term average spreads (OAS adjusted to exclude the months encompassing the global financial crisis and early COVID-19 period), as seen in Figure 1 and 2. For instance, the credit spread on B-rated debt currently is slightly more than 200 bps below its long-term average, seen as –2.10% in Figure 1, which is comparable to lows touched in 2007 and 1997 — periods that preceded the global financial crisis (2008), the meltdown of Long-Term Capital Management Fund (1998) and the Dot-Com crash (2000), respectively. The same pattern is true of BB-rated debt. This is not to suggest that markets are at the precipice of an adverse event or development, but rather that history shows us in retrospect that adverse events often are preceded by periods of market complacency, which can last a couple of years. Credit markets currently are showing better discipline with CCC debt, where credit spreads are below the long-term historical average but are nowhere near the negative levels reached in 1997, 2007 and even 2021 (Figure 2). Credit investors are being more discerning with this lowest-rated cohort but are piling into debt rated BB and B. Whether these high-yield credit allocations prove to be merely aggressive or reckless won’t be known for a while, but current money flows to low-rated issuers likely will put a ceiling on the potential for restructuring activity through 2025.

Figure 2: CCC Rated Option-Adjusted Spread Minus LT Average

Source: FRED, the Federal Reserve Bank of St. Louis

That said, large Chapter 11 filings and other restructuring activity remain at elevated levels through May, with 31 large (>$50 million) filings just in the last two months and the speculative-grade default rate near 5.0%. Comparisons of restructuring activity to the year-to-date 2023 period are down about 20%, mostly attributable to a weak start to 2024, but overall a respectable showing considering the strength of last year’s first-half totals. Financial markets continue to see the glass as half-full; they seem undaunted by a resolute Fed, the implications of persistently high interest rates on the leveraged corporate sector and fairly robust levels of restructuring activity. This current dynamic can’t go on intact much longer, but it’s not obvious what’s going to give first.

Footnotes:

1: J.P. Morgan Leveraged Finance (May 28, 2024).

2: Hanna Ziady, “Billionaires Jamie Dimon and Ray Dalio sound the alarm on soaring US government debt,” CNN Business (May 16, 2024).

3: J.P. Morgan Leveraged Finance (May 28, 2024).

4: “S&P 500 Earnings and Estimate Report,” S&P Global (May 14, 2024).

5: Daniel Kreps, “Kiss Sell Music Catalog, Publishing and Imagery to Company Behind ABBA Voyage,” Rolling Stone (April 4, 2024).

Related Insights

Related Information

Published

June 12, 2024

Key Contacts

Key Contacts

Global Co-Leader of Corporate Finance & Restructuring